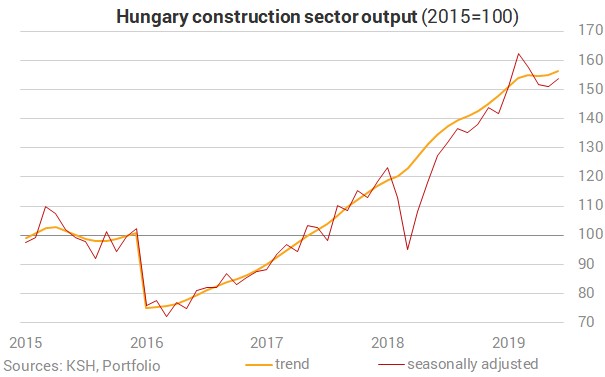

The volume of construction output in Hungary grew by 1.7% month on month in June 2019. As the Central Statistical Office (KSH) recorded contraction in the preceding three months, this is only a minor correction. This shows that the amazing speed at which the sector was expanding has diminished quite a lot in the second quarter, but on an annual basis the sector’s contribution to economic growth remains significant.

As you can see on the charts below, the performance of the construction sector (on a seasonally adjusted basis) worsened after a peak in February, but the ascending trend was not broken.

On an annual basis, the volume of construction output was still up by 20%, i.e. the June performance is far from being weak. The volume of output increased in both main groups of construction: in the construction of buildings by 23.5%, in civil engineering works by 16.5%. In the construction of buildings, the increase was due to industrial and warehouse constructions (mainly relating to state projects financed from EU funds); in civil engineering projects, road, railway and utility constructions generated the growth.

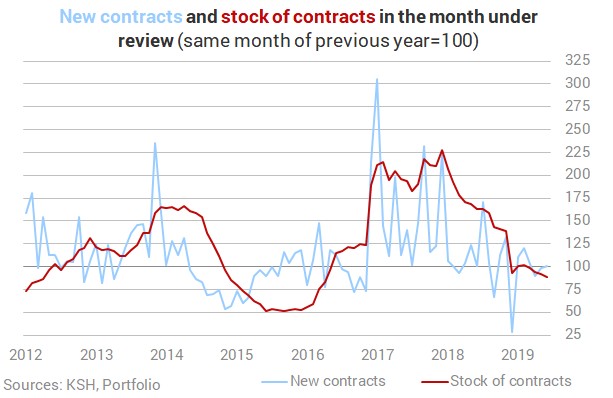

At the same time, the momentum of the sector is likely to fade even further. This assumption is underpinned by the fact that the stock of new contracts has practically stagnated (+0.9%). Whereas the volume of new contracts concluded in the construction of buildings went up by 27.4%, in the construction of civil engineering works the volume lessened by 12.6% year-on-year. The latter might suggest that the contracts of large state projects co-financed by the European Union have already passed their peak, and in the current EU fiscal cycle we should probably expect a decrease (until 2022-2023).

As a result of the humble growth in the stock of new contracts and the constantly rising base, the volume of the stock of contracts at construction enterprises was down 11.2% yr/yr at the end of June.

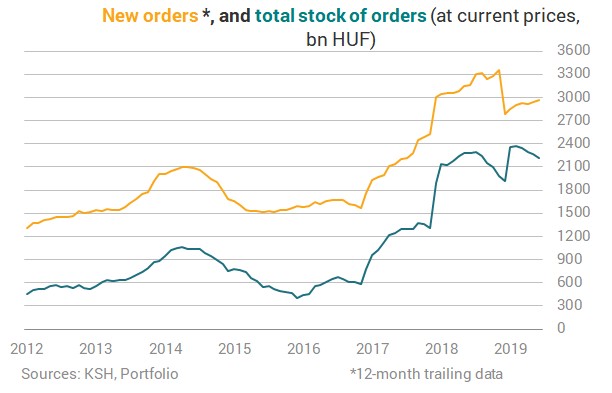

We should not expect much of a contraction in output, though, since the stock of orders fell from a high base and it remains at an elevated level.

As regards the second-quarter performance of the construction sector, the pattern is very much like the one shown by the ‘big brother’ industrial sector. The sector was unable to improve its performance in the second quarter, but its contribution to GDP growth could remain significant on an annual basis. We estimate this contribution to be over 0.5%, i.e. the small-weight sector remains a key engine of economic growth.